Last year was full of unexpected events – from a regional banking crisis, to rising geopolitical risks, to skyrocketing mortgage rates – that ultimately led to a solid year for markets and a recession that never came. The events that unfolded in 2023 once again showed that there are no crystal balls that allow investors to see the future clearly. Thus, when building a financial plan, a wide range of potential outcomes must be considered, with investors being willing and able to accept the downside risks. Here are the top 10 lessons for investors.

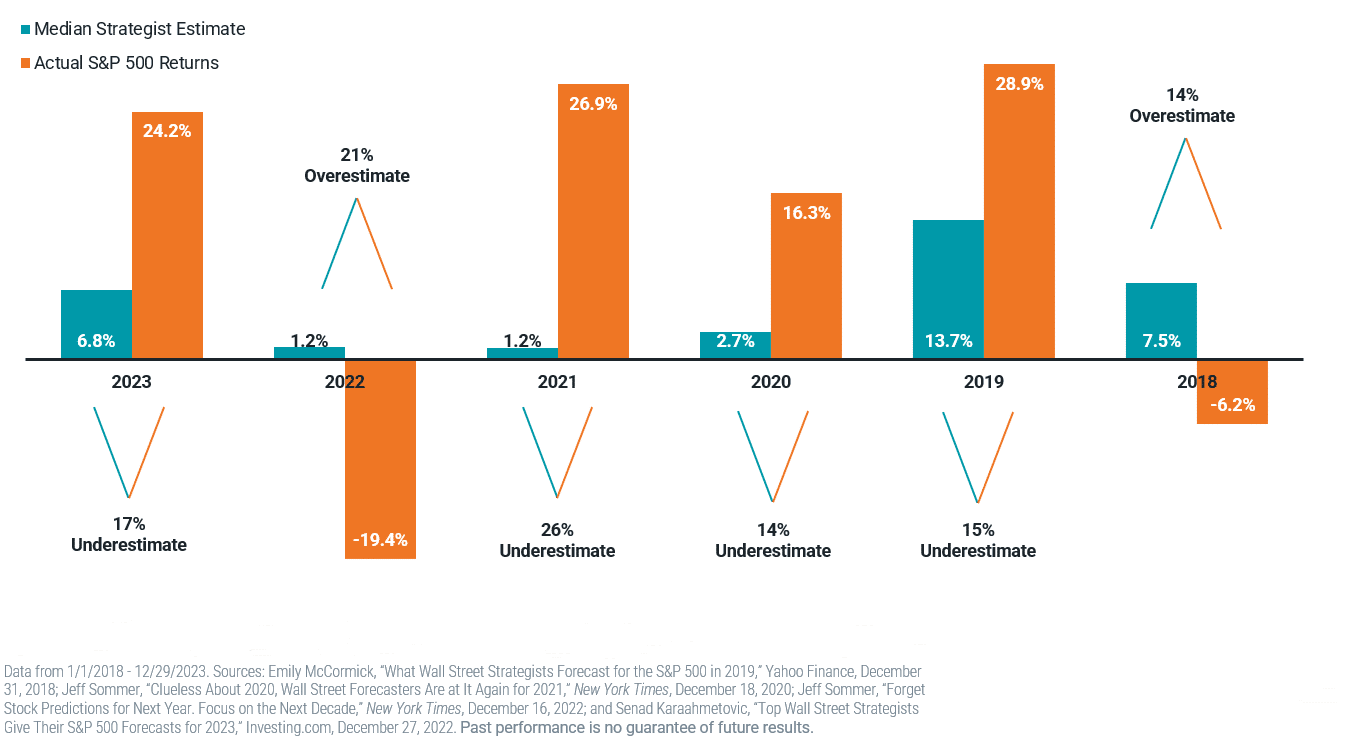

When it comes to market predictions, anything can happen. In fact, the only value in market strategists’ forecasts is that they show many outcomes are possible. The S&P 500’s performance is a case in point. At the start of 2023, the predictions of 23 analysts from leading investment firms ranged widely. Some thought the index would end the year down 5%, others up 24%, and the average forecast was for it to end up 6%. Defying these expectations, it closed the year up 26.4%, a surprise for many, especially those that expected 2023 to be a difficult year for investors.

Consensus S&P 500 Estimates vs. Actual Returns (2018-2023)

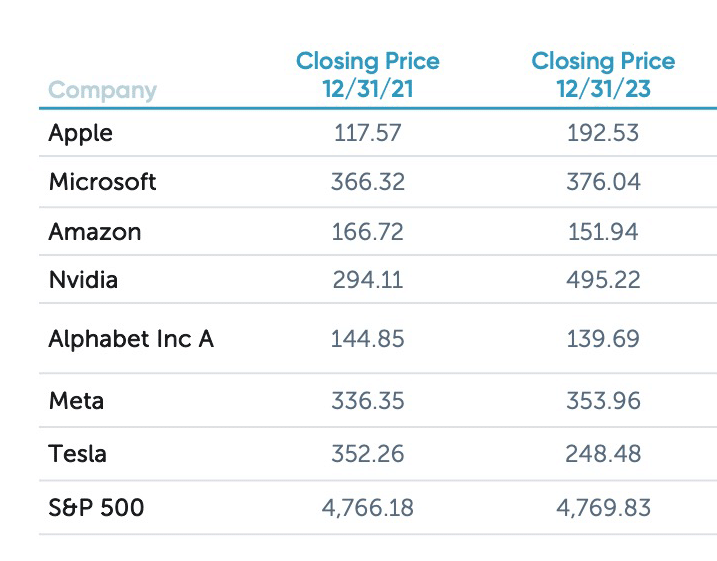

The S&P 500’s better-than-expected performance was greatly impacted by investors’ fascination with the rise of artificial intelligence in the tech sector, turning into perhaps the biggest trending story of the year. The Magnificent Seven tech stocks were largely responsible, accounting for more than 62% of the S&P 500’s performance. History provides cautionary warnings about sky-high valuations driven by stories. Those seven tech stocks’ valuations are now reminiscent of the Nifty 50 and the dotcom stocks just before crashing. While not a forecast, investors should keep in mind that it is difficult for highly valued companies to continue to outperform over the long term. Fortunately, the rest of the market has valuations much closer to their historical averages.

Magnificent Seven Stocks 2021 and 2023 Closing Prices

Market strategists commonly try to predict future stock returns by looking at equity valuations. One popular measure is the cyclically adjusted price-to-earnings (P/E) ratio, known as the Shiller CAPE 10. The problem with timing the market based on the CAPE 10 is that history shows it leads to a wide range of possible outcomes. The CAPE 10 was 28.3 at the end of 2022 – well above the historical average of about 17, suggesting valuations were historically high. When it gets too high, investors not focused on the long term might begin to panic. This was part of the reason many predicted a poor year for stocks in 2023.

In 2023, we saw a turnaround for some of the unique risk assets that recently endured a period of poor performance – particularly with reinsurance funds, a type of alternative investment. Investors who dropped these funds from their portfolios when performance soured missed out on the comeback. The only way investors can benefit from diversifying their portfolios to include unique risks, such as value stocks, international stocks and alternative investments, is to recognize that every risk asset will likely experience long periods of underperformance. That likelihood is why we diversify across many different assets instead of concentrating risks in one or a small group. To get the full benefits of diversification, you must have the discipline to stay the course, rebalancing a portfolio instead of allowing yourself to be subject to recency bias.

When risk assets have poor returns, it is usually because they are experiencing both poor performance – through lower earnings or losses – and falling valuations. Because the best predictor we have of future equity returns is the earnings yield (the inverse of the P/E ratio, or E/P), falling valuations mean that future expected returns are now higher. Investors subject to recency bias fail to understand that, leading them to sell instead of buying. The lesson for investors is to remember that self-healing mechanisms are at work after periods of poor performance. Thus, sophisticated investors know that the winning strategy is to avoid market timing, but if you cannot resist, you should “be fearful when others are greedy and be greedy only when others are fearful,” as Warren Buffett advised.

Imagine that on Jan. 1, 2023, you were given a crystal ball that would enable you to see the major geopolitical and economic events of the coming year. Given those facts, it’s hard to imagine that any investor would have predicted that the S&P 500 would rise 26.4%. And it is likely that many investors would have sold equities based on the negative news that was coming. The lesson is that even if you could accurately predict events, you should not try to time markets based on forecasts.

Headlines and predictions surrounding the 2024 presidential election ramped up last year, especially as the Republican presidential primary field began shrinking. While reading these stories, remember that investors often make mistakes because they are unaware that their beliefs and biases influence their decisions. The first step to preventing such mistakes is to become aware of how our views impact our choices. Studies show that people’s optimism toward both the financial markets and the economy is dynamically influenced by their political affiliation and the existing political climate. So, ignoring your political views when making investment decisions is one lesson that rears its head after every presidential election. Remember to express your views with your votes, not with your investments.

From January through October, small-cap stocks performed poorly. For example, the Vanguard Russell 2000 ETF (VTWO) – which predominantly invests in stocks of small U.S. companies – produced a return of -4.4%, and the Avantis Small Value ETF (AVUV) – which invests in a broad set of U.S. small-cap companies – returned just 0.8%. Both far underperformed Vanguard’s S&P 500 Index ETF (VOO), which invests in stocks in the S&P 500 and returned 10.6% during that period. Impatient, undisciplined investors and those subject to recency bias may have abandoned investments in small-cap stocks. Using Portfolio Visualizer’s back-testing tool, we find that over the next two months, while VOO returned 14.2%, VTWO returned 22.4%, outperforming by 8.2%, and AVUV returned 21.9%, outperforming by 7.7%. Patience and discipline, not performance chasing, are necessary ingredients for investment success.

The historical evidence demonstrates that individual investors are performance chasers – they buy yesterday’s winners (after the great performance) and sell yesterday’s losers (after the loss has already been incurred). This causes investors to buy high and sell low – not a recipe for investment success. As I wrote in my book, The Quest for Alpha, that behavior explains the findings from studies that show investors can underperform the very mutual funds they invest in.

Last year was another in which most active fund managers failed to beat their benchmarks, even though the industry claims active managers outperform in bear markets. In addition to the advantage of being able to switch to cash, active managers had a great opportunity to take advantage of the large dispersion in returns between the best and worst stocks in 2023. Unfortunately, investors in active funds continue to pay for the triumph of hope over wisdom and experience.

Every investor makes mistakes. However, smart investors don’t repeat the same mistakes and expect different outcomes. By utilizing the 10 lessons 2023 taught us, you can avoid making common investment errors. It’s also important to know your financial history and have an investment plan backed by evidence. If you don’t have a strategy, read my book “Investment Mistakes Even Smart Investors Make and How to Avoid Them”.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third-party sources, which may become outdated or otherwise superseded without notice. Third-party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Total return includes reinvestment of dividends and capital gains. Mentions of securities are to demonstrate passive funds versus active funds, and low-cost funds. The mentions of specific securities should not be construed as recommendations of securities. Performance is historical and past performance is not an indication of future results. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements, or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability, or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this article. R-24-6678

The content of this article was written by a third party, not an employee of Northwest Wealth Management.

Larry Swedroe | Head of Financial and Economic Research @ Wealth Advisor at Buckingham Strategic Partners

As Head of Financial and Economic Research, Larry Swedroe has authored or co-authored 16 financial books and devotes all of his time to research and education in the areas of investing, financial planning and behavioral finance.